Private real estate 101

Key Takeaways

Commercial Real Estate

Primary Strategies

Main Drivers

What is commercial real estate?

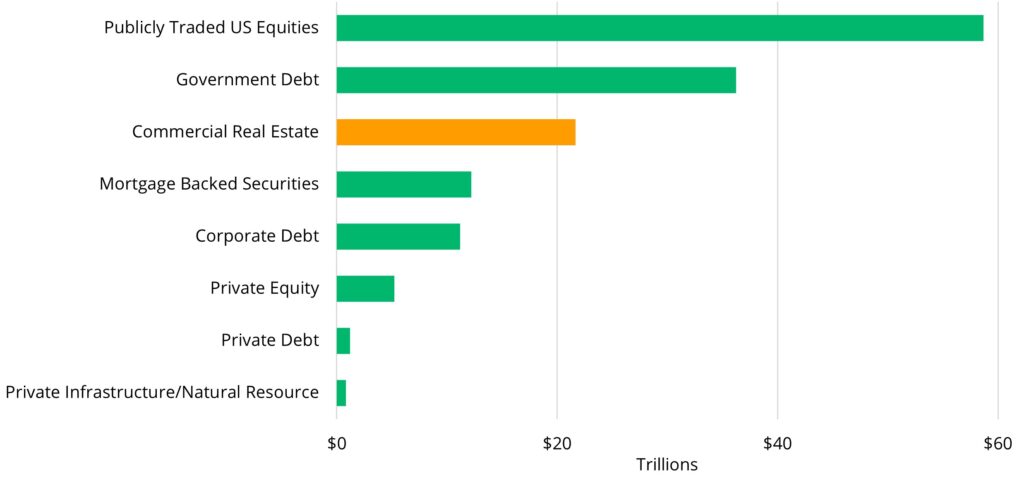

Commercial Real Estate Ranks as the Third Largest Asset Class in the USii

Major CRE Sectors

Rental residential broadly includes any form of housing that is not owner-occupied, including apartments, low-density, and single-family rentals, Seniors housing, and student housing.

Industrial encompasses manufacturing facilities as well as warehouses and distribution centers that store physical goods.

Office buildings house firms and workers who are primarily engaged in services activities, such as administration, management, finance, and information.

Retail refers to physical (or “brick and mortar”) stores, which could take various formats, such as malls, neighborhood shopping centers, restaurants, and convenience stores.

Hospitality refers to the hotels, resorts, and similar locations that offer overnight lodging.

Primary CRE Investment Strategies

Private CRE Fundraising Over the Past Five Years Was Heavily Concentrated in Value-Added and Opportunistic Strategiesiii

Private CRE as an Asset Class

Private real estate has an established track record of delivering investment returns through business cycles as highlighted below.

Private CRE Has Recorded Low Correlations with Stocks and Bonds Since 2000iv

|

Private CRE |

Public CRE |

Stocks | |

|---|---|---|---|

|

Public CRE |

0.18 | ||

|

Stocks |

0.04 |

0.70 | |

|

Bonds |

-0.14 |

0.24 |

-0.09 |

CRE managed by private investment managers provides investors with exposure to real assets, typically compiled in a fund or a private REIT that own or intend to acquire large portfolios of single-sector or diversified property types. Investment managers specialize in real estate management and oversee day-to-day asset management on behalf of their investors.

Public CRE investment vehicles are traded on stock exchanges and offer liquidity just as any other publicly traded security. Investors may note that Public CRE securities can be influenced by swings in broader market sentiment. In Private CRE, there are typically longer-duration commitment periods, and investors may expect higher potential returns as a ‘liquidity premium’ as a trade-off for liquidity.

Private CRE is the dominant form of investment in real assets as Public CRE accounts for less than 10% of the CRE transaction market.v

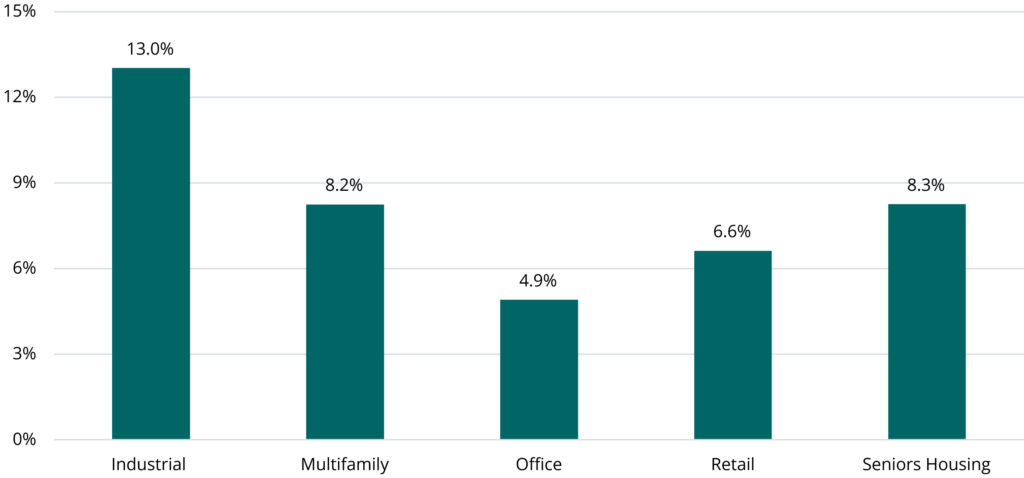

Private CRE has Delivered Healthy Annual Returns over the Past 15 Yearsvi

Explore Private Markets Further

Explore select private market asset classes to understand better what they are, who uses them, and the potential to identify value.

Explore Private Real Estate Asset Classes

Explore select private market asset classes to understand better what they are, who uses them, and the potential to identify value.

© 2025 Bridge Investment Group Holdings LLC. “Bridge Investment Group” and certain logos contained herein are trademarks owned by Bridge.

The information contained herein is for informational purposes only and is not intended to be relied upon as a forecast, research, investment advice or an investment recommendation. Reliance upon the information in this material is at the sole discretion of the reader. Past performance is not necessarily indicative of future performance or results.

This material has been prepared by the Research Department at Bridge Investment Group Holdings LLC (together with its affiliates, “Bridge”), which is responsible for providing market research and analytics internally to Bridge’s strategies. The Research Department does not issue any independent research, investment advice or investment recommendations to the general public. This material may have been discussed with or reviewed by persons outside of the Research Department.

This material does not constitute an offer to sell any securities or the solicitation of an offer to purchase any securities. This material discusses broad market, industry, or sector trends, or other general economic, market, social, legislative, or political conditions and has not been provided in a fiduciary capacity under ERISA.

Economic and market forecasts or estimated returns presented in this material reflect the Research Department’s judgement as of the date of this material and are subject to change without notice. Although certain information has been obtained from third-party sources and is believed to be reliable, Bridge does not guarantee its accuracy, completeness, or fairness. Bridge has relied upon and assumed without independent verification, the accuracy and completeness of all information available from third-party sources. Some of this information may not be freely available and may require a subscription or a payment. Any forecasts or return expectations are as of the date of material and are estimated and are based on market assumptions. These assumptions are subject to significant revision and may change materially as economic and market conditions change. Bridge has no obligation to provide updates or changes to these forecasts.

This material includes forward-looking statements that involve risk and uncertainty. Readers are cautioned not to place undue reliance on such forward-looking statements. Any reference to indices, benchmarks, or other measure of relative market performance over a specified period of time are provided for context and for your information only.

i US Census Bureau, American Community Survey 1-Yr. Estimate, 2022.

ii Low-Income Housing Tax Credits (LIHTC) are a federal program that incentivizes private developers to create or rehabilitate affordable rental housing for low-income households by providing them with tax credits.

iii Section 8 is a federal housing assistance program that provides rental subsidies to low-income households, either through vouchers or project-based assistance.

iv AMI determines the thresholds for eligibility to receive housing assistance and can vary widely by market.

v US Census Bureau, American Community Survey 1-Yr. Estimate, 2010-2022.

vi RealPage, as of Q2 2024.

vii US Census Bureau and the Department of Housing and Urban Development (“HUD”), 2021 American Housing Survey: Housing Costs - Renter-occupied Units (created by the AHS Table Creator).

viii US Census Bureau and the Department of Housing and Urban Development (“HUD”), 2021 American Housing Survey: Housing Costs - Renter-occupied Units (created by the AHS Table Creator).

ix US Census Bureau and the Department of Housing and Urban Development (“HUD”), 2021 American Housing Survey: Housing Costs - Renter-occupied Units (created by the AHS Table Creator).

x US Census Bureau & Department of Housing & Urban Development, American Housing Survey, 2021.

xi National Housing Preservation Database, Picture of Preservation, 2021.

xii National Housing Preservation Database, Picture of Preservation, 2021.

xiii CoStar, as of Q2 2024.

xiv CoStar, as of Q2 2024.

xv Engineering News-Record via Moody’s Analytics, Baseline Scenario, as of Q2 2024.

xvi Center on Budget and Policy Priorities, Low-Income Housing Tax Credit Could Do More to Expand Opportunity for Poor Families, 28 August 2018.

xvii Engineering News-Record via Moody’s Analytics, Baseline Scenario, as of Q2 2024.

ON THIS PAGE...